Middle East tensions are likely to weaken the Asia Pacific economy

The abundance of oil resources in the Middle East makes this region have a strong influence on world geopolitics.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

The following article was translated using both Microsoft Azure Open AI and Google Translation AI. The original article can be found in Ketegangan Timur Tengah Rentan Melemahkan Ekonomi Asia Pasifik

Smoke billows out during the Israeli bombing in Rafah in southern Gaza Strip on October 19, 2023. Thousands of people, both Israeli and Palestinian citizens, have died since October 7, 2023, when the Palestinian Hamas organization based in the Gaza Strip launched a sudden attack into southern Israel, causing Israel to declare war against Hamas in Gaza on October 8th.

The Middle East conflict is prone to causing global economic instability. The abundance of petroleum resources makes this region have a strong influence on world geopolitics. Many countries are dependent on oil supplies from this region, including the Asia Pacific region, including Indonesia.

The ongoing armed conflict between Hamas and Israel is feared to trigger a wider conflict that could increase the vulnerability in the Middle East region. The involvement of several countries on each opposing side could potentially cause a conflict that disturbs the distribution of oil worldwide. Especially if the conflict causes disputes between Arab countries, which ultimately trigger tension in the Persian Gulf, the Gulf of Oman, and around the Eastern Mediterranean Sea.

The waters in that area are highly vulnerable to being affected by the geopolitical conflict, which would have an impact on the distribution of oil exports that pass through the sea route. Maritime blockades could potentially occur when certain countries use their geopolitical power to defend the side they support.

The worry is based on the diplomatic relationships of several Arab countries that are close to the United States. In addition, some Arab countries have now made peace with Israel, such as the United Arab Emirates, Bahrain, Sudan, Morocco, Jordan, and Egypt. Even Saudi Arabia, as the leader of Gulf countries, is increasingly close to efforts to restore diplomatic ties with Israel.

The situation is likely to be exploited by the US and its allies to gain support from a number of Arab countries to "soften" their stance towards Israel's actions. This will certainly strengthen the geopolitical position of the US and its allies to support and send military aid to Israel. On the other hand, there are several countries in the Middle East region that remain steadfast in supporting the resistance of Palestinian fighters, such as Iran, Lebanon, and Syria.

These three countries have maritime boundaries as their territorial borders, thus allowing them to use their geopolitical power to influence the course of warfare, such as Iran which has sea borders with the Persian Gulf to the Oman Sea and Lebanon along with Syria which has sea borders in the Eastern Mediterranean.

Also read: Opening the World's Eyes to the Humanitarian Threat in Palestine

An Israeli artillery shell exploded above a house in Al-Bustan, a border village between Lebanon and Israel, southern Lebanon, on October 15, 2023.

Tensions in the Persian Gulf and Gulf of Oman regions have the potential to disrupt the distribution of energy from Kuwait, Saudi Arabia, Bahrain, Qatar, the United Arab Emirates, Oman, Iraq and Iran, which could trigger prices energy surged. Likewise, disturbances in Eastern Mediterranean waters could trigger an increase in the price of distribution of goods and services from Europe to the Middle East, especially those passing through the Suez Canal in Egypt, becoming more expensive.

The lack of solidarity among Arab states can lead to conflicting interests in supporting their respective camps. This is very vulnerable to triggering wider tensions and can have an impact on the distribution of crude oil and its derivative products globally. If this happens, it will create economic turmoil caused by skyrocketing prices of global crude oil.

The cost of shipping goods and services will become more expensive, thus exposing the finances of oil-importing countries to erosion in order to patch up the increasingly expensive energy subsidy on the international market. If oil-importing countries fail to allocate sufficient funds, the option to reduce subsidies by raising the price of fuel is a rational choice to rescue their finances. However, fiscal measures such as this may ultimately trigger higher inflation, lower the purchasing power of the public, decrease economic growth, and make unemployment and poverty more prevalent.

Middle East Oil

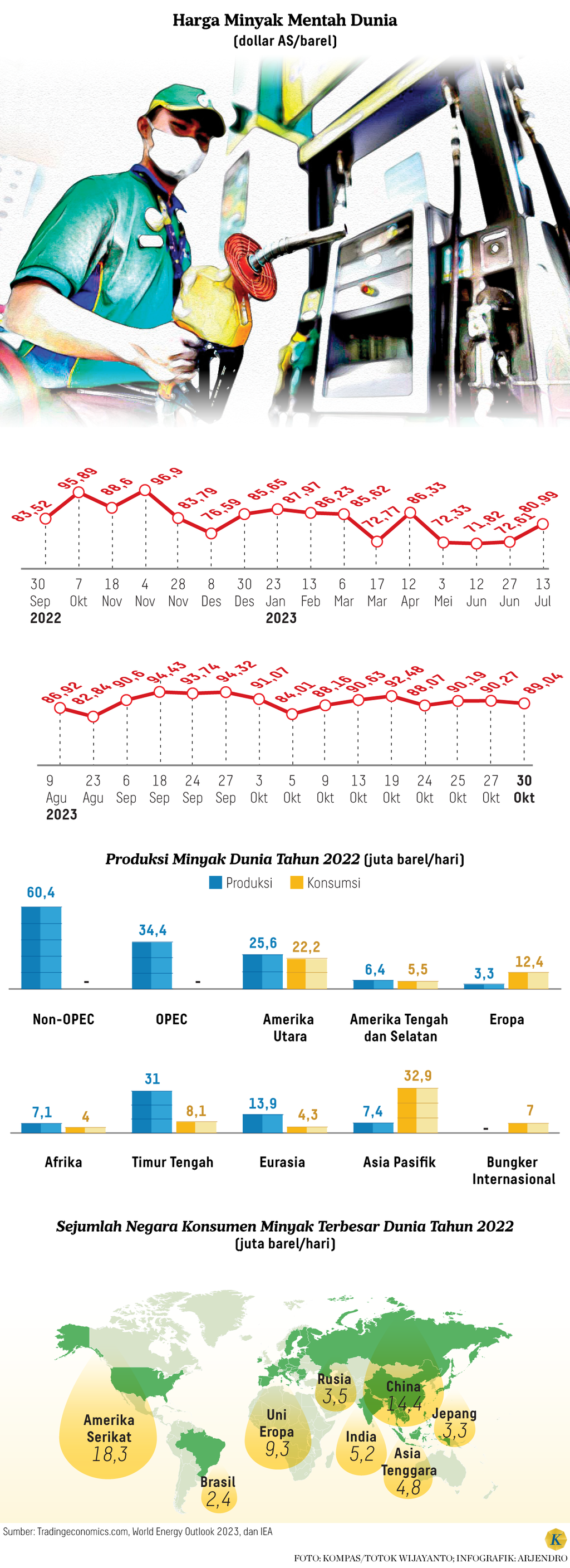

In the petroleum trade, the Middle East plays a crucial role in stabilizing global market supplies. Based on data from the International Energy Agency (IEA) in 2022, this region's crude oil production reached 31 million barrels per day. Out of this production, only about 8 million barrels per day are absorbed within the region, resulting in a surplus of 23 million barrels of oil production per day in the Middle East.

The surplus is the largest among other oil-producing regions. Take, for example, the North American region, which has a surplus of around 3 million barrels per day; Central and Southern America have almost 1 million barrels per day; Africa ranges at about 3 million barrels per day; and Eurasia has an average surplus of around 9 million barrels per day.

Also read: Measuring the Potential Economic Impact of the Hamas-Israel Crisis

The surplus production of over 20 million barrels per day of oil in the Middle East has made this region a crucial backbone to the energy market equilibrium worldwide. Any decrease in oil production or disruption in oil shipment from this region will have widespread impacts on international energy commerce.

Therefore, even though Palestine and Israel are not world oil producers, the geopolitical elements of the Middle East region that accompany them can trigger energy scarcity due to political interests. This is highly risky for all countries in the world, especially those with minimal fossil energy resources.

The financial burden borne by oil-poor countries will be increasingly burdensome with the soaring prices of oil in the global market. Each country must devise strategies to deal with this situation by implementing its fiscal and monetary policies appropriately according to their respective conditions, in order to avoid economic stagflation in the country in question.

There are two regions in the world that are highly vulnerable to the macroeconomic situation of the commodity of crude oil: Europe and the Asia Pacific region. Both of these regions are classified as areas with minimal energy supply from their internal territories, so they must import fossil energy from outside the region. Every day, these two regions always have a large deficit in energy supply. Europe experiences a shortage of about 8 million barrels per day, while the Asia Pacific region has a deficit of around 25 million barrels per day. Such a situation makes both regions have a very low level of energy sovereignty because their level of dependence on foreign sources is very high.

The shortage of oil supply can be a vulnerability for both regions in the global geopolitical game. Naturally, both regions are relatively easy to "control" and regulate in order to meet their domestic energy supply.

Asia Pacific

There are a number of countries in the Asia Pacific region whose level of dependence on oil energy supply is very high. These countries are China, India, Japan, and countries in Southeast Asia. The average oil consumption levels in these four regions are above 3 million barrels per day. In fact, China's daily consumption rate reaches 14.4 million barrels, ranking second in the world after the US with a consumption rate of 18.3 million barrels per day.

However, China is more vulnerable compared to the US as it mainly relies on foreign imports for its oil energy supply. China's daily oil production is only around 4 million barrels, so it needs to import about 10 million barrels of oil per day. Unlike the US, which can meet its energy consumption from domestic production and still have a surplus to export overseas.

Also read: The Western World's Double Standards for Israel's Attack on Gaza

A container is seen at a port in Nanjing in the eastern province of Jiangsu, China on October 27, 2022.

As a result, the world's largest commodity importer of crude oil is currently occupied by China. It can be imagined that if there is a global situation that affects the price of crude oil in China's market, it will indirectly affect the international trade balance as well. This is because China plays a central role in the trade of several important commodities that are needed worldwide.

Therefore, the continuous upward trend of world oil prices since the Israel-Hamas conflict erupted on October 7, 2023 should be closely monitored, especially for net importing countries like Indonesia. This is particularly important if the price increase trend lasts for a relatively long time and exceeds the estimated Indonesian Crude Price (ICP) scenario. In the 2023 state budget, the ICP for this year is estimated to be around 90 US dollars per barrel, so any oil price hikes exceeding the ICP benchmark must be closely monitored and addressed to avoid a heavy burden on the country's finances.

Currently, the price of crude oil has been hovering around $90 US dollars per barrel since the beginning of September 2023. This situation is driven by high demand from several countries, including China. At the same time, the supply from oil-producing and exporting countries in the world (OPEC) has slightly decreased, which has led to a more expensive price increase.

The unfinished supply-demand problem is now being exacerbated by the Israeli-Palestinian geopolitical conflict which is heating up the geopolitical situation in the Middle East. There is the potential for diplomatic relations to become vulnerable which could trigger world oil prices to soar even more expensively. Therefore, the role of all countries in the world, including Indonesia, is urgently needed to mediate this conflict so that it quickly subsides and maintains global geopolitical and geoeconomic stabilization. (COMPAS R&D)