Year-End Notes on Fintech

The balance on goods and services recorded a surplus in recent months. The deficit in the state budget, which is projected to continue to decline in 2021 and 2022, is expected to maintain the exchange rate stability.

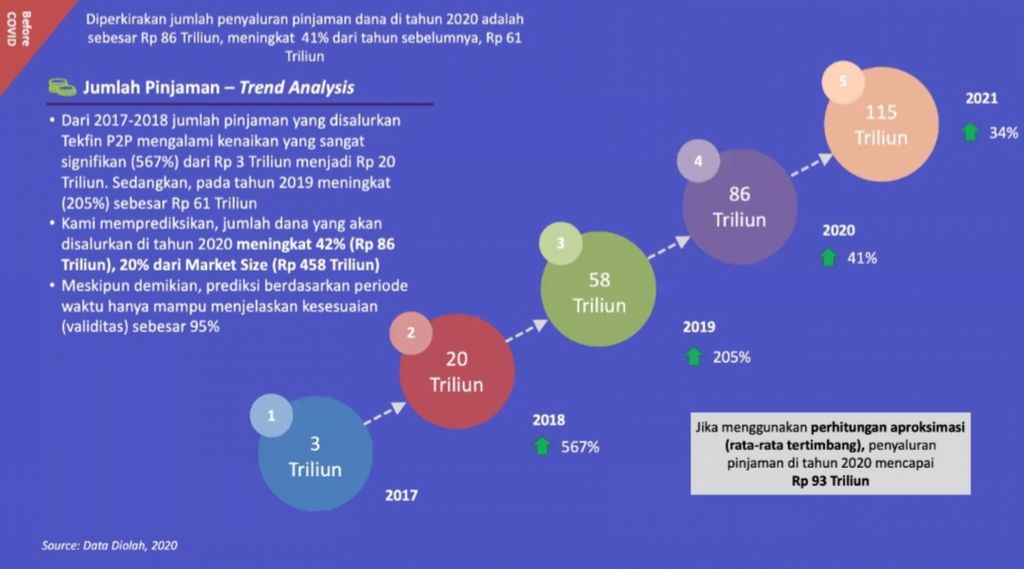

The trend of increasing the amount of financing disbursed by inter-party financing fintech providers.

The easing of the Covid-19 pandemic has brought optimism that economic growth will accelerate in 2022. Although there is a risk of the tightening of monetary policy in the United States, good communication from the Federal Reserve, the US central bank, is expected to maintain the stability of global financial markets.

Also read:

> Bridging the Financial and Real Sectors

> Maintain Commitment in Economic Recovery Plan

The balance on goods and services recorded a surplus in recent months. The deficit in the state budget, which is projected to continue to decline in 2021 and 2022, is expected to maintain the exchange rate stability. Fiscal discipline must be maintained so that the government debt ratio can be gradually lowered to levels recorded before the pandemic.

The gross merchandise value (GMV) of Indonesia's digital sector in 2021 is estimated to reach US$70 billion with a 49 percent growth on an annual basis.

The pandemic has become an opportunity for digital economic growth. According to the e-Conomy SEA 2021 report published by Google, Temasek and Bain & Company, from the beginning of the pandemic up until the first half of 2021, there were 21 million new digital consumers in Indonesia. The data show that 72 percent of the new consumers did not come from big cities. The gross merchandise value (GMV) of Indonesia's digital sector in 2021 is estimated to reach US$70 billion with a 49 percent growth on an annual basis.

There are at least seven factors that play a role in the significant increase in digital economic growth in 2021. First, related to the rapid expansion of the digital ecosystem. Now, Indonesia has eight unicorns, the second most in ASEAN countries.

The growing need for funding can make an initial public offering (IPO) an attractive option for unicorns or start-ups in Indonesia to raise funds.

To support this, the Financial Service Authority (OJK) has issued a regulation on multiple voting shares (MVSs) as a strategic step to accommodate unicorns and start-ups to conduct IPOs.

The 2019 Fintech Summit Expo press conference on the lending fintech industry, on Tuesday (24/9/2019), in Jakarta.

One of Indonesia's unicorns, Bukalapak, recorded the largest fundraising in the history of the stock exchange, reaching Rp 21.9 trillion (US$1.53 billion). However, learning from the fall in Bukalapak's stock price, there is a need to educate retail investors about the stock valuation of start-up companies. Retail investors should also have a medium-term investment perspective, not just on a short-term basis.

Second, the rising trend of the acquisitions of small banks by technology companies. The presence of neobanks (online banks) and the digital transformation by conventional banks should be welcomed. However, like conventional banks, the challenge for digital banks is to find cheap funds and increase total assets.

Learning from digital banks in other countries, such as KakaoBank in South Korea and MYbank (ANT Group) in China, one of the keys to a neobank's success is the construction of a digital ecosystem that is

integrated with financial technology (fintech), e-commerce or ride hailing. The OJK has responded positively to this development by issuing a regulation on commercial banks and a regulation on services and products provided by commercial banks that clarifies the definition of a neobank.

Third, the achievement of the digitization target of 12 million merchants through the QRIS code. We should appreciate the performance of Bank Indonesia (BI) and the payment system industry, which includes payment fintech. Another initiative in the BI pipeline is the National Open API Payment Standard (SNAP), which will enter the implementation phase in 2022. The Open API is expected to accelerate collaboration between banks and fintech as well as the digital economy ecosystem.

Fourth is the use of digital technology in government-to-person (G2P) payments such as in the distribution of social assistance. Digitalization can reduce the potential for misuse in social assistance distribution such as by eliminating intermediary issues that are often a source of inefficiency in the distribution process.

This success can be used as a benchmark in the distribution of the social assistance program through fintech.

By the end of 2021, internet and smartphone user penetration in Indonesia is expected to reach 72.8 percent and 72.1 percent, respectively. Indonesia should be proud of its successful record with the Pre-Employment Card program. This success can be used as a benchmark in the distribution of the social assistance program through fintech.

Fifth, the development of peer-to-peer (P2P) lending fintech. Based on OJK data, as of last November, as many as 104 P2P lending fintech platforms were licensed and registered with the OJK, with the number of lender and borrower accounts reaching 749,000 and 68 million, respectively, while the value of the total fund distribution and fund outstanding reached Rp 249 trillion and Rp 26 trillion, respectively. The collaboration between banks and P2P lending platforms also showed improvement. However, the presence of illegal online lenders, popularly called pinjol, remains worrying. All stakeholders need to continue to maintain the credibility of P2P lending platforms by eradicating the illegal operations.

P2P lending rates also need to be lowered. Now, the average interest rate has declined 0.8 percent to 0.4 percent per day. Generally, people borrow money from online lenders for consumption with a short tenor. This interest rate, if calculated on an annual basis, can reach 146 percent per year. This interest must be lowered again so that more people can benefit from the P2P lending ecosystem.

Modem devices used by online loan businesses are illegal.

Sixth, the role of e-investment in capital market democratization. The development of digitalization in capital market products has proven to successfully answer the issue of financial inclusion in Indonesia. As of October 2021, the number of capital market investors increased to 6.8 million from 3.9 million in 2020. Mutual fund investors increased to 5.8 million from 3.2 million in 2020 and Government Securities investors increased to 588,000 from 460,000 in 2020.

In order to continue to increase the number of investors, it is necessary to consider the implementation of registration requirements using a simpler "e-KYC" approach to facilitate the development of retail investors with a relatively small investment value, according to the risk profile of potential investors, but still prioritizing the prudence principle.

Finally, the need for data for innovation has also raised new challenges. Both the private and government sectors, as parties that collect and manage data, are vulnerable to the risk of breaches and misuse of personal data. The ratification of the Personal Data Protection Bill is urgently needed.

Indonesia must be able to take the maximum advantage of the development of the digital economy, not only for the sake of promoting financial inclusion, but also for accelerating the pace of the economic recovery. Digital literacy must be improved. In formulating policies, the most important thing is the application of principle based regulation and the principle of balance between the need for innovation and consumer protection.

MIRZA ADITYASWARA, an economist and the chairman of the Indonesia Fintech Society (IFSOC)

(This article was translated by Hendarsyah Tarmizi).