Fiscal dominance locks monetary policy because it must reduce inflation and maintain market growth and stability.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

By

AGUSTINUS PRASETYANTOKO PENGAJAR UNIKA ATMA JAYA JAKARTA,

·5 minutes read

KOMPAS/TOTOK WIJAYANTO

Governor of Bank Indonesia, Perry Warjiyo (third from left) and his team prepare to start a press conference on the results of the Governor Council Meeting (RDG) of Bank Indonesia in Jakarta, on Thursday (21/12/2023). BI maintains its benchmark interest rate at 6 percent.

The Board of Governors meeting Bank Indonesia in April 2024 decided to increase the BI Rate by 25 basis points to 6.25 percent. Many people, including me, did not expect BI to raise interest rates so quickly. It seems that the pressure on (exchange rate) stability is too strong that interest rates need to be raised immediately.

Pressure on the rupiah has increased since the United States central bank (The Fed) decided to hold the benchmark interest rate at 5.25-5.50 percent. In his speech, Fed Chair Jerome Powell said the price increase in the first three months of 2024 was faster than expected at 2.7 percent or still higher than the target of 2 percent.

Initially, it was predicted that The Fed's interest rates would drop at least three times throughout 2024, starting in June or July. In the new scenario, even if there is a decrease in interest rates, it will only happen once in September or December 2024. Global investors are readjusting their investment composition by increasing their placement in assets denominated in US dollars.

As a consequence, investment returns (yield) in US dollars increased to reach their highest level since 2007, reaching 4.5-4.6 percent for bonds with a maturity of ten years.

That is why the US dollar index rose to its highest level in the past 20 years. On April 29, 2024, the dollar index reached 105.73 after reaching 112 in September 2022, which was the highest since December 2001 at 116.

Every time the US dollar index rises, asset prices in US dollars fall due to high demand. As a consequence, investment returns (yield) in US dollars increased to reach the highest level since 2007, reaching 4.5-4.6 percent for bonds with a maturity of ten years.

AFP/GETTY IMAGES/GETTY IMAGES NORTH AMERICA /CHIP SOMODEVILLA

The Governor of the United States Federal Reserve, Jerome Powell, attended a press conference at the William McChesney Martin building on March 20, 2024, in Washington, DC, USA.

The dynamics of the market have put pressure on the exchange rate of the rupiah, which reached Rp 16,270 per US dollar at the end of April 2023, the lowest since 2020. The yield of 10-year maturity rupiah bonds has increased again, reaching 7.2 percent.

Similarly, the Composite Stock Price Index (IHSG) on the Indonesia Stock Exchange (IDX) continues to be under pressure and has even dropped below 7,000. In situations like this, policy of raising the benchmark interest rate is inevitable. Moreover, Bank Indonesia's monetary policy focus is to maintain stability.

Only with stability can stalled global economic activity be revived.

In a conference commemorating the 50th anniversary of the founding of the Basel Committee, the global banking and financial sector supervision committee under the coordination of the Bank of International Settlement (BIS) concluded that stability (of the financial sector) is a global public good (global public good ).

Only with stability can the stalled global economic activities be restarted. This conclusion has important implications as it will become the direction of monetary and financial authorities' policies worldwide.

This conclusion is drawn after observing the phenomenon of global economic and geopolitical structural changes where inflation has become the most serious threat that must be addressed by many countries, particularly developed countries.

SALOMO TOBING

A Prasetyantoko

Four conclusions

There are four main conclusions that were drawn from the conference. First, the importance of stronger supervision over banks and other financial institutions.

Second, placing the issue of operational resilience as a new risk that is important to mitigate due to various problems. This ranges from geopolitics, cyber attacks, to climate change.

Changes in the geopolitical constellation have forced many countries to strengthen their defenses again (remilitarization).

Thirdly, anticipating changes in market structure caused by various structural factors. Fourthly, focusing on capital and global liquidity issues as implications of the increasing global debt ratio.

Changes in the geopolitical constellation have forced many countries to strengthen their defenses again (remilitarization). Meanwhile, climate change demands greater allocation of funds for adaptation and mitigation in the face of various climate related risks. Not to mention that many countries in the world tend to be populist so they need large budgets to finance social programs.

AFP/SAUL LOEB

The issue of air pollution is not new. The community has been threatened by air pollution for a long time. Numerous research studies demonstrate the impacts of air pollution, but unfortunately, significant efforts to control air pollution have yet to be taken. Consequently, residents are increasingly suffering from the effects of air pollution.

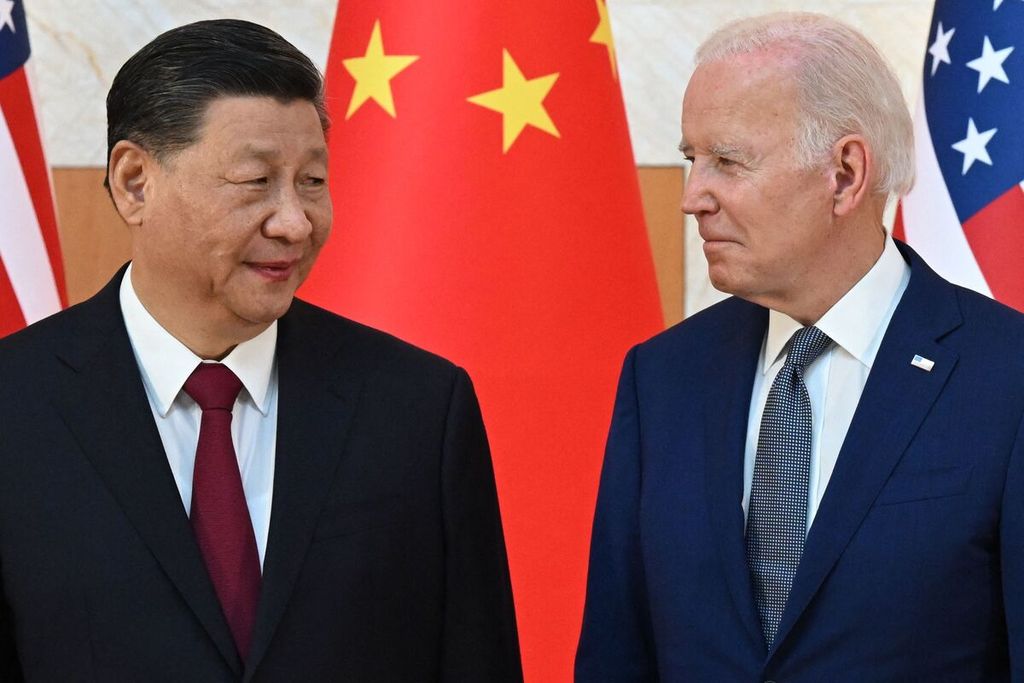

The President of the United States, Joe Biden (right), and the President of China, Xi Jinping, met during the G20 Summit in Nusa Dua, Badung Regency, Bali on November 14, 2022. The competition between the two superpowers, the United States and China, has an impact on the global economy.

Increased funding needs, whether due to remilitarization, climate change, or populist programs, will drive up debt, which in turn will increase global liquidity. The more liquidity, the more vulnerable the economy is to crises. Moreover, the cost of issuing debt is higher due to rising interest rates.

In fact, this issue has been studied in depth by Hyman Minsky through his theory of the evolution of finance fromhedge,speculative, to ponzi. A (big) crisis will occurs because slowly but surely and often without realizing it, the financial behavior of economic agents shifts from being prudent (hedge) to being reckless (speculative) and ultimately fatal (ponzi).

The moment where turmoil is inevitable due to shifts in financial behavior is called the "Minsky Moment".

In the short term, the risk of recession can be avoided, but that does not mean it disappears completely.

The quarterly report of the International Monetary Fund, the Global Financial Stability Report April 2024 edition, sees debt issues, both government and private, as a significant source of risk in the medium term. Although the economic prospect is improving, inflation remains high, and debt risks need to be monitored closely.

In the short term, the risk of recession can be avoided, but it doesn't mean it disappears altogether. It is possible that it may return in the future, triggered by high levels of debt.

KOMPAS/NINA SUSILO

Finance Minister Sri Mulyani Indrawati (second from the right), Bank Indonesia Governor Perry Warjiyo (second from the left), Chairman of the Financial Services Authority (OJK) Commissioner Council Mahendra Siregar (far right), and Chairman of the Deposit Insurance Corporation (LPS) Commissioner Council Purbaya Yudhi Sadewa (left) left Merdeka Palace, Jakarta, on Monday (23/10/2023) after a meeting related to financial system stability.

Medium term risks

This warning is relevant to our economy, especially regarding the new government's work program starting in October 2024. One of the challenges of political regimes in many countries is to avoid excessive populist approaches as they will create fiscal burdens that will exacerbate the worrying global capital and liquidity structures.

If fiscal discipline is abandoned, for whatever reason, the risks can be fatal. Fiscal dominance has made monetary policy locked because it must address three things at the same time, namely dampening inflation, maintaining economic growth, and creating market stability.

Fiscal dominance has locked monetary policy as it has to address three things at once, namely damping price increases (inflation), maintaining economic growth, and creating market stability.

That's the trilemma as a new challenge for monetary authorities around the world. BI's latest decision to raise interest rates in order to calm the market shows this policy trilemma.

The government's future work program should prioritize the increase of economic productivity as the strongest defense against future economic turbulence. Programs that indirectly boost productivity need to be reassessed to avoid creating risks in the future.

Editor:

FX LAKSANA AGUNG SAPUTRA

Share

Kantor Redaksi

Menara Kompas Lantai 5, Jalan Palmerah Selatan 21, Jakarta Pusat, DKI Jakarta, Indonesia, 10270.

Tlp.

+6221 5347 710

+6221 5347 720

+6221 5347 730

+6221 530 2200

Kantor Iklan

Menara Kompas Lantai 2, Jalan Palmerah Selatan 21, Jakarta Pusat, DKI Jakarta, Indonesia, 10270.