Three Challenges Threaten Indonesia's Financial Stability

Financial system stability faces three challenges. One of them, global uncertainty. What else?

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

Deputy Governor of BI Juda Agung gave a speech at the launch of the 42nd Financial Stability Study book titled "Encouraging Increased Intermediation Amid Global Uncertainty" in a hybrid event in Jakarta on Wednesday (27/3/2024).

JAKARTA, KOMPAS – In the midst of global uncertainty, three challenges confront the country's financial stability. In this situation, Bank Indonesia remains focused on maintaining macroeconomic stability and financial system.

Deputy Governor of BI, Juda Agung, conveyed this when delivering a speech at the launch of the Financial Stability Study Number 42 book entitled "Encouraging Intermediation Improvement in the Midst of Global Uncertainty", in a hybrid manner, in Jakarta, on Wednesday (27/3/2024).

Based on a study on the risk of financial system stability, Indonesia faces three major challenges. These challenges include global uncertainty, digitalization risk, and the risk of transitioning towards a green economy.

The United States (US) interest rate is one of the factors that causes uncertainty in the global economy and financial markets.

Juda said that the level of interest rates in the United States was one of the factors causing uncertainty in the global economy and financial markets. Even though the prospect of the US Central Bank (The Fed) interest rate is expected to begin to decline, the timing of the execution and the impact of the reduction in interest rates is still a big question mark.

In the end, this policy will affect capital flows to developing countries, including Indonesia.

"In addition, geopolitical tensions in various parts of the world have not shown any signs of ending. This development is then exacerbated by the increasing fragmentation of global trade, especially since global political policies can change drastically, considering that currently 50 percent of the world's population are holding general elections, including in the US," he said.

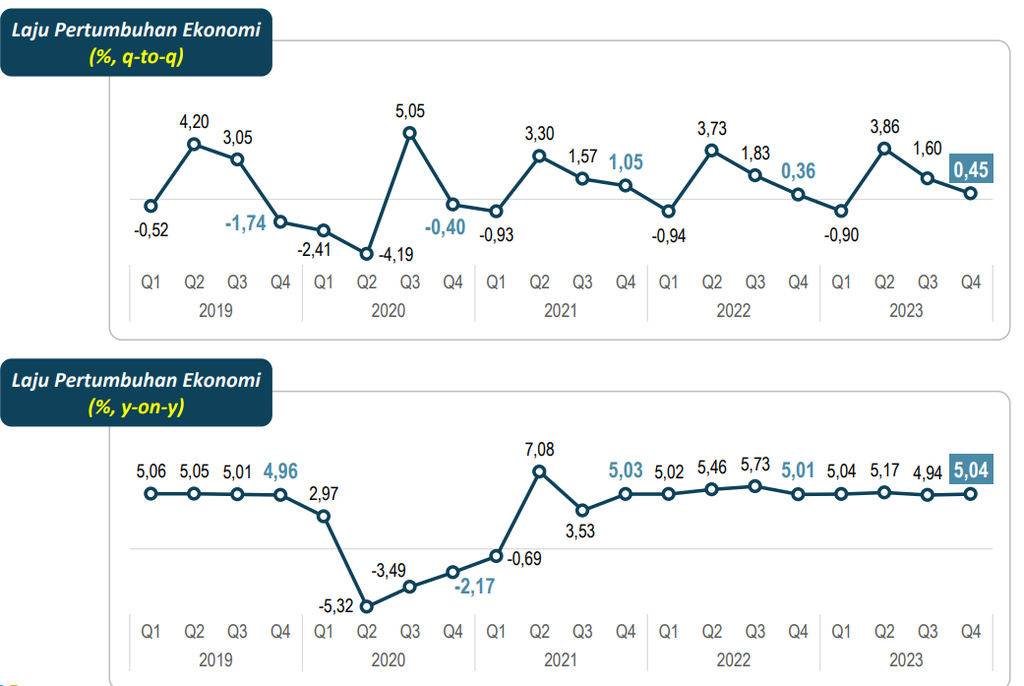

Economic growth rate from 2019-2023 on a quarterly basis. Source: Central Statistics Agency

Financial digitalization

The second risk, as Juda continues, is related to financial digitalization. Although it can expand access to financial inclusion, digitalization also brings new risks, namely cyber security.

The cyber threat to financial institutions can endanger the stability of the financial system due to disrupted operations, theft of personal data, and manipulation of financial transactions.

Also read: Not Optimal Dividend and Credit Targets

Therefore, according to Juda, financial institutions need to implement strong cybersecurity measures, increase cyber awareness, and invest in technology and human resources to anticipate cyber threats. Collaboration between financial institutions, regulators, and related parties is also important in managing cyber risks.

"The last risk is green economic risk. In this case, the banking sector face risks including, firstly, transition risks related to policies on reducing carbon emissions such as carbon tax. Secondly, credit risks related to debtor's ability to adapt to changes in the market and green economic policies. Thirdly, reputation risks," he said.

We believe that with the growth in DPK, we will return to normal this year, as well as with the high liquidity of banking instruments, we predict our credit growth to be around 10-12 percent.

In facing these three challenges, BI will remain focused on maintaining macroeconomic and financial system stability. This is done by implementing monetary policy that aims at stability (pro-stability), while macroprudential policy is focused on economic growth (pro-growth).

Apart from that, BI is currently finalizing policies related to cyber security as a whole (end-to-end) and increasing credit distribution to inclusive and green sectors. All of these efforts aim to maintain financial system stability amidst global conditions full of uncertainty.

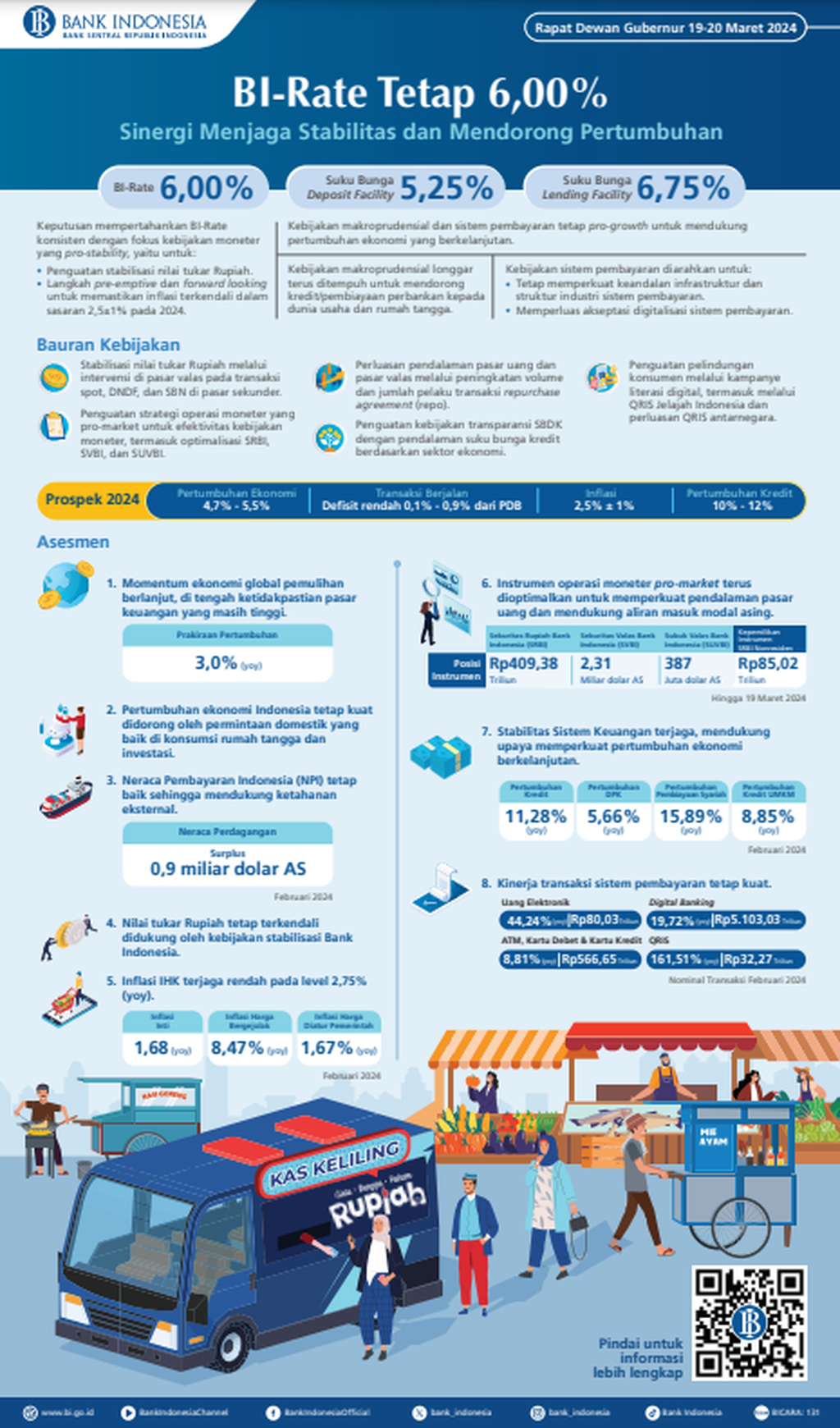

Infographic shows the results of the March 2024 Bank Indonesia Board of Governors Meeting and various aspects of the domestic economy.

Domestic challenges

Amidst the high levels of global uncertainty, the stability of Indonesia's financial system is well-maintained, reflected by adequate liquidity, decreasing credit risks, and strong capitalization. The resilience of the financial sector is also supported by good corporate resilience which contributes to the continued stability of the domestic financial system.

As of February 2024, the bank credit distribution grew by 11.28% annually, supported by the banks' liquidity availability and the credit demand from the business world. Meanwhile, the banks' liquidity reflected by the ratio of liquid instruments to third-party funds (AL/DPK) is still sufficient, at a level of 27%.

"We believe that with the growth of demand deposits, we will return to normal this year and with the high level of bank liquid instruments, we estimate our credit growth to be around 10-12 percent," said Juda.

As of February 2024, credit disbursement by banks is expected to grow by 11.28 percent annually supported by the availability of bank liquidity and credit demand from the business world.

The gathering of bank deposits is currently slowing down, reaching an annual level of 3.73 percent in December 2023, far below the level of credit distribution at that time which touched an annual level of 10.38 percent. However, the gathering of deposits in January 2024 began to grow again by 5.8 percent annually, with credit growth reaching 11.83 percent.

Residents are displaying Indonesian rupiah that has been exchanged at the mobile Bank Indonesia booth at O2 Corner, Palmerah Selatan, Jakarta, on Tuesday (26/3/2024).

DPK slows down

Secretary of the State-Owned Banks Association (Himbara), Achmad Solichin Lutfiyanto, stated that the slowdown in Third Party Funds (DPK) is positively correlated with the broad money supply (M2). Therefore, DPK growth in 2024 is estimated to slow down.

"This trend of slowing deposits occurred throughout the balance tiering, which was somewhat stable in the middle class, but the balance of the lower class fell drastically, even the balance of the upper class also fell. "That only leaves the middle class, which is now being fought over by all the banks," he said in the discussion session.

The balance of lower class society fell drastically, even the balance of upper class society also fell.

Regarding credit distribution, continued Achmad, there has been an increase in the number of credit facilities to customers who have not yet been withdrawn at the bank (undisbursed loans) by around two-fold in 2023. This condition will improve in line with the level of investor confidence in the prospects Indonesian economy.

According to Achmad, the growth of credit distribution and TPF the banking industry was also influenced by Himbara's performance. From the previous period, growth in Himbara's credit distribution and TPF was recorded as being above the banking industry, around 12 percent and 4.65 percent respectively on an annual basis.

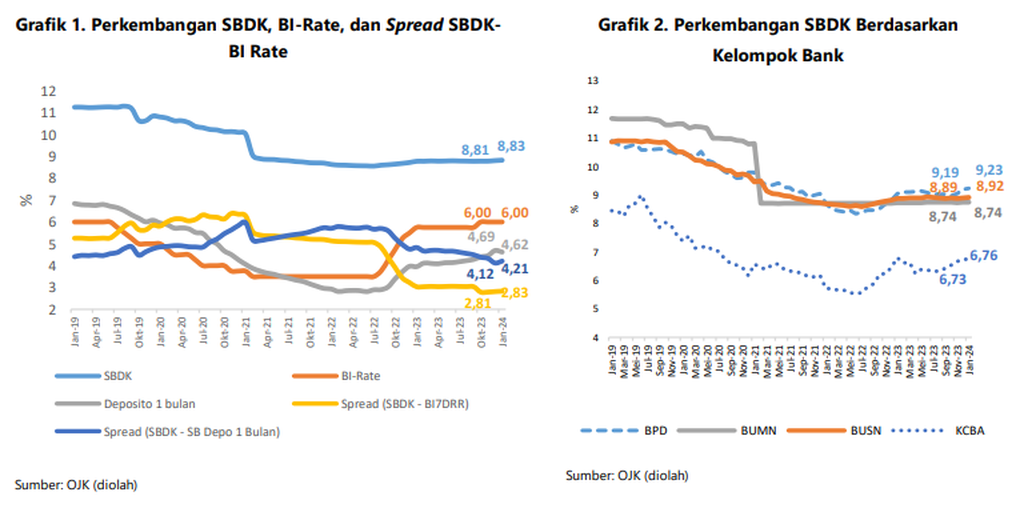

The graph shows the development of SBDK, BI-Rate, and SBDK BI Rate Spread as well as the development of SBDK based on bank groups until January 2024.

"Indeed, Himbara is the driveroutside of its assets which reach 50 percent of total national banking assets. Apart from that, talking about intermediation, this also has risks. NPL (nonperforming loan) is starting to be controlled, but LAR (loan at risk) is also high. "If it is not managed, (LAR) will fall to NPL in 2024," he said.

Nevertheless, Achmad assessed that the national banking industry is relatively resilient to various risks, supported by adequate reserves for impairment losses (CKPN) and NPL coverage.

Furthermore, the growth of credit in the banking industry can reach 10-12 percent as targeted by the government if Himbara is able to achieve double-digit growth.

Also read: BI Consistently Holds Interest Rates at 6 Percent

There are four things that need to be considered to achieve the target, namely improving asset quality with strong reserves, sufficient liquidity, sufficient capital, and searching for new sources of growth.

Thus, the banking industry still has the potential to grow according to targets amidst conditions of global uncertainty and domestic challenges.