Consumer Protection and Digital Finance

As other countries have implemented, Indonesia needs to use a risk-based approach in regulating the digital finance industry. This will help adapt regulations on rapidly developing technologies.

MIRZA ADITYASWARA

Adapt or die. Perhaps this is how we can describe the impact of digitalization on life today. Many people initially resisted digitization, but it was inevitable.

A few indicators show its positive impact in encouraging economic growth and financial inclusion in Indonesia. Investment in digital companies has been growing rapidly in Indonesia. According to a 2021 survey conducted by Alpha JWC Ventures and Kearny, the total value of Indonesia’s investments in digital companies reached US$4.4 billion in 2020, double that compared to the 2019 figure.

By 2025, there will be a three- to sixfold increase in digital transactions in nonmetropolitan cities. On the one hand, it is a business opportunity, but the increase in the United States’ interest rates will make investors more selective about investing their funds.

Like the two sides of a coin, apart from being proven to drive economic growth and financial inclusion, digitalization also presents new challenges. One of these is related to consumer protection, such as the increased risk of fraud and financial crimes. Therefore, amidst rapid developments in the digital economy, risk mitigation efforts should be strengthened further.

Also read:

> Increasing Inflation and Economic Recovery

> Falling into Loan Sharks’ Traps

According to the Organisation for Economic Co-operation and Development (OECD), consumer protection risk in the digital age is driven by four factors. First is risk from market activities, including the use of illegal products and the emergence of new types of fraud. Second is risk that stems from regulatory and supervisory effectiveness of in keeping up with technological developments.

Third is risk that stems from the level of consumer awareness and knowledge, especially vulnerable people. Last is technology risk. Not all companies have the same cybersecurity standards.

A World Bank report published in April 2021 offers concrete examples of consumer protection efforts that financial technology (fintech) companies can make in microfinancing, online lending, crowdfunding, and electronic money (e-money). Digital microfinancing platforms can implement price and fee transparency. Meanwhile, online lending platforms must apply a conducive approach in dealing with debt collection.

The Financial Services Authority (OJK) should further strengthen its efforts in eradicating illegal lenders. Meanwhile, crowdfunding fintechs can determine limits on investment value based on a consumer’s profile. Finally, e-money must separate customer funds from corporate funds and strengthen cybersecurity.

Officers serve customers who want to increase their electronic money balance at the Ovo outlet in a shopping center in the Kebayoran Lama area, South Jakarta, Friday (11/29/2019). Nowadays, the use of electronic money is increasingly popular.

Illegal investments

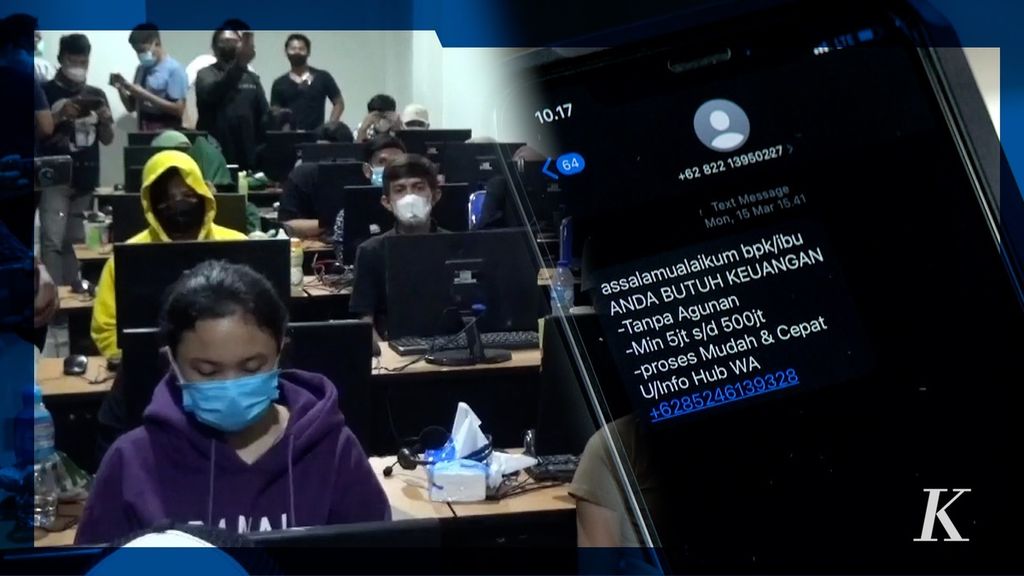

Along with the rapid development of Indonesia’s digital economy, illegal investments are emerging under the guise of digital companies offering a variety of products, from illegal online loans to illegal binary options. Cases of illegal online loans are mushrooming in Indonesia. As of March 2022, the Investment Alert Task Force (SWI) has closed 3,889 illegal online lenders. Now, there are only 102 lenders that are licensed by the OJK.

In debt collection, many borrowers have been threatened and intimidated by debt collectors. Some borrowers reportedly committed suicide as a result of threats and intimidation. The victim's family and relatives were also threatened using their contact information stolen from the victim's mobile devices.

There have also been a number of cases of fraud using Ponzi schemes via social media platforms and instant messaging applications. The perpetrators collected public funds under the pretext of investment, crowdfunding, and arisan (tontine) schemes that promised high returns. The victims were tempted to increase their contributions because of the promise of high returns, and then the perpetrator disappeared. Many people have been deceived by such illegal investment schemes.

Also read:

> Problem of Investment Literacy

> Investor Protection Should be a Priority

The latest fraud cases are online scams involving illegal binary options and illegal trading bots that have resulted in many victims.

Such platforms often use influencers or affiliates in a strategy to demonstrate their wealth to attract potential investors. According to the National Police, one platform that illegally offered binary options caused up to Rp 97 billion ($618.50 million) in losses to consumers.

According to the SWI, the total loss incurred by illegal investments in the last 10 years reached Rp 117 trillion. Fraud can take place due to technological advancements that allow illegal investment schemes to be offered easily through social media platforms or instant messaging applications. Meanwhile, the reality is that people are not very familiar with investment products.

The Investment Alert Task Force closed 50 illegal online lending entities and 21 illegal investment entities from the beginning of 2022 to the present. They are closed to prevent consumers from being caught in a loss.

Consumer protection

A single institution cannot handle consumer protection amid the rapid digitalization of the financial sector. This issue must be addressed by regulators, industry, and the public. Therefore, three steps can be taken.

First, it is necessary to strengthen supervision over the digital finance ecosystem through collaboration, both as a preventive measure, such as special supervision of digital finance influencers and technological curative steps in handling consumer complaints.

A number of measures have been introduced, such as Cekrekening.id of the Communication and Information Ministry and Cekfintech.id of the Indonesian Fintech Association (Aftech). The social media platforms and instant messaging applications that fraudsters often use should also play an active role in dealing with fraud.

As other countries have implemented, Indonesia needs to use a risk-based approach in regulating the digital finance industry. This will help adapt regulations on rapidly developing technologies.

Second, it is necessary to increase digital and financial literacy among the public, including micro, small, and medium enterprises (MSMEs). Regulators, together with industry players, need to intensify public education efforts on digital and financial literacy and financial products in order to prevent online fraud. Times have changed, so digital finance influencers also need to be educated, considering the big role they play in influencing society.

Finally, it is necessary to strengthen regulations to provide security, build trust and prevent fatalities in extreme cases. These are related, for example, to passing the personal data protection bill currently being discussed at the House of Representatives (DPR). In addition, certification should be required for digital finance influencers who frequently offer investment advice.

As other countries have implemented, Indonesia needs to use a risk-based approach in regulating the digital finance industry. This will help adapt regulations on rapidly developing technologies.

MIRZA ADITYASWARA, Steering Committee of the Indonesian Fintech Society (IFSOC).

(This article was translated by Hendarsyah Tarmizi.)