At the same time, the mobility restrictions that cause economic disruption have made people lose their income and companies experience a decline in profits.

By

James P. Walsh

·5 minutes read

Since the onset of the Covid-19 pandemic, millions of people have died of Covid-19 in various parts of the world. However, this pandemic constitutes not only a tragedy of humanity, but also an economic tragedy.

Many countries have adopted mobility restriction policies to prevent virus transmission. Nevertheless, such policies are like a double-edged sword that also hampers economic activities, deprives many people of their livelihood, and causes the business sector to face uncertainty over when the economy and demand can return to their pre-pandemic vigor.

In facing the challenges of the pandemic, governments across the world are striving to maintain public health and ascertain the availability of jobs. Extraordinary policies have been introduced by many countries, including Indonesia.

Tax incentives, guarantees, loans for small-scale businesses and direct public assistance are the policies that various countries have chosen.

Also read:

Debt and Growth

At the same time, the mobility restrictions that cause economic disruption have made people lose their income and companies experience a decline in profits. Consequently, government incomes from taxation have declined so budget deficits have grown. In order to cover deficits, governments need to expand their budgets through debt financing, among other measures.

Still safe

In Indonesia, the government has increased the state budget to support health facilities, testing and tracing, vaccine supplies, business incentives and direct assistance to affected people.

Countries all over the world encountered the same challenge and made the same choice. Is this the right choice? For Indonesia, the answer is yes. The current nominal ratio of Indonesian debts is indeed higher than that in 2019. But by observing the current condition and the projection fir future economic activities, the International Monetary Fund (IMF) sees that Indonesia’s debt ratio generally remains safe.

The IMF makes routine economic assessments of all its members, a process in which one part is to determine members’ debt management capacity. In this case, the IMF does not rely on a certain threshold.

The IMF has noticed that each country has distinctive conditions and prospects. For instance, a country with an increasing debt ratio due to investments in the new and renewable energy sector will find it easier to access financing sources in the future. But a country that increases debt excessively during an economic boom tends to experience pressure on its debt repayment when the growth rate starts to moderate.

DEWI INDRIASTUTI

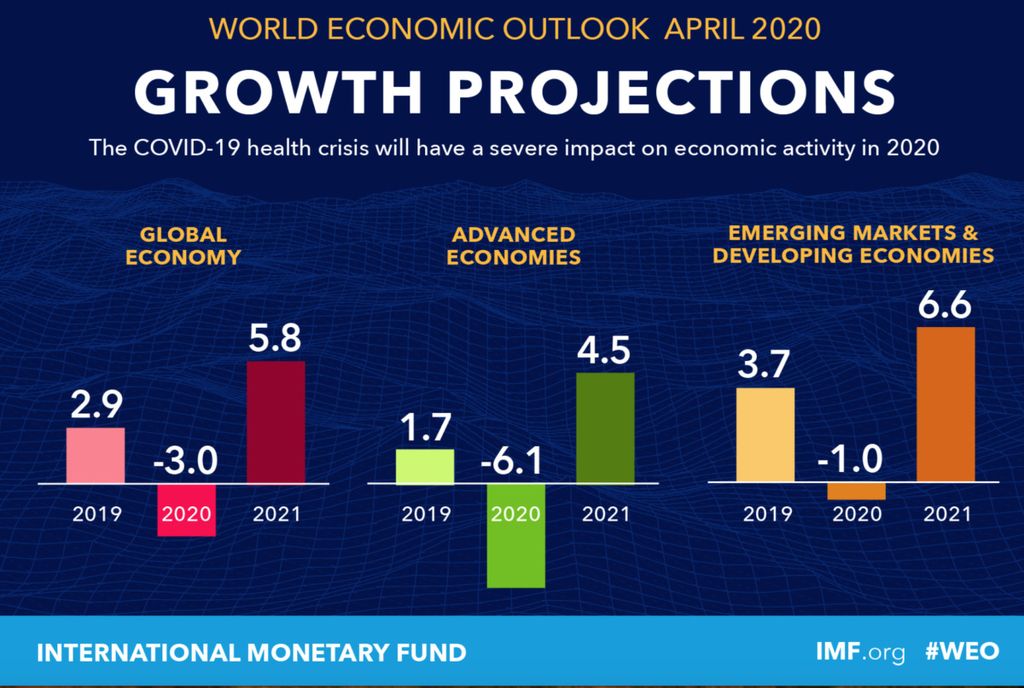

IMF projections for April 2020

In an October 2021 IMF report, due to be revised in early 2022, the IMF estimates that the Indonesian government’s debt-to-gross domestic product (GDP) ratio has increased from about 30.6 percent at the end of 2019 to 36.6 percent in 2020. At the end of 2021, the ratio was estimated to reach 41.4 percent.

The Indonesian government is simply capable of managing the debt ratio properly and prudently.

At a glimpse, this ratio indeed seems high, but in view of the present condition, the debt-to-GDP increase has resulted from the policy that many other countries also shared. The Indonesian government is simply capable of managing the debt ratio properly and prudently.

This is reflected in several developments. First, the Indonesian economy has been fairly stable, even during the pandemic. Second, the pressure from the outflow of foreign funds that happened last year has subsided and the Indonesian financial market has again recorded inflows that helped its foreign exchange reserves reach a relatively high level.

Third, Indonesia’s present cost of debts is not higher than pre-pandemic levels. Unlike many developing countries, international rating institutes have not lowered Indonesia’s credit worthiness. The global community, especially investors, still retains optimism for the Indonesian economy.

No complacency

Yet, this does not mean that Indonesia can be complacent. When the economy recovers, tax receipts are expected to increase again in line with the endorsement of the Law on Harmonization of Tax Regulations (UU HPP).

On the other hand, extraordinary spending will automatically decrease. Indonesia now possesses a strong framework for managing the state budget (APBN). Before the Covid-19 pandemic, Indonesia was already capable of maintaining its budget deficit at no more than 3 percent of GDP, a policy that indicates discipline and prudence.

Although Indonesia’s current budget deficit is higher, the macro condition as reflected in Indonesian inflation is still under control and the rate of economic growth has begun to indicate recovery. Assuming that recovery continues and no new problems arise related to Covid-19, the IMF sees that Indonesia’s budget deficit can return to less than 3 percent of GDP in 2023 as outlined in the government road map.

In another sphere, from now until 2023 Indonesia leads the G20, the multilateral cooperation forum with member countries that belong to the world’s largest economies.

KOMPAS/MUHAMMAD SAMSUL HADI

Turkey’s President Recep Tayyip Erdogan addresses the virtual G20 Leaders’ Summit in Riyadh, Saudi Arabiain, in a video conference from his Vahdettin Pavilion, in Istanbul, Sunday, Nov. 22, 2020. Erdogan said Sunday that Turkey sees itself as a part of Europe, but he called on the European Union to “keep your promises” on issues such as the country’s membership bid and refugees.

This forum offers opportunities for member countries to discuss the latest economic policies and issues. Indonesia’s prudent fiscal policy management and its commitment to curb deficits is an interesting and innovative topic.

The IMF will continue to cooperate with Indonesia. Through a constructive relationship, the IMF will keep learning from Indonesia and convey other countries’ experience in policy implementation to Indonesia.

James P. Walsh,Senior Resident Representative for Indonesia, International Monetary Fund (IMF)