Deflation Amid Threat of Recession

The threat of an economic recession in Indonesia is not without its foundational reasons. Amid the threat of recession, deflation was also recorded in July.

Office workers wearing face masks enter a building during lunch time in the financial business district in Singapore on August 11, 2020. - Singapore\'s virus-hammered economy shrank almost 43 percent in the second quarter, in a sign that the country\'s first recession in more than a decade was deeper than initially estimated, official data showed on August 11.

The threat of an economic recession in Indonesia is not without its foundational reasons. Amid the threat of recession, deflation was also recorded in July.

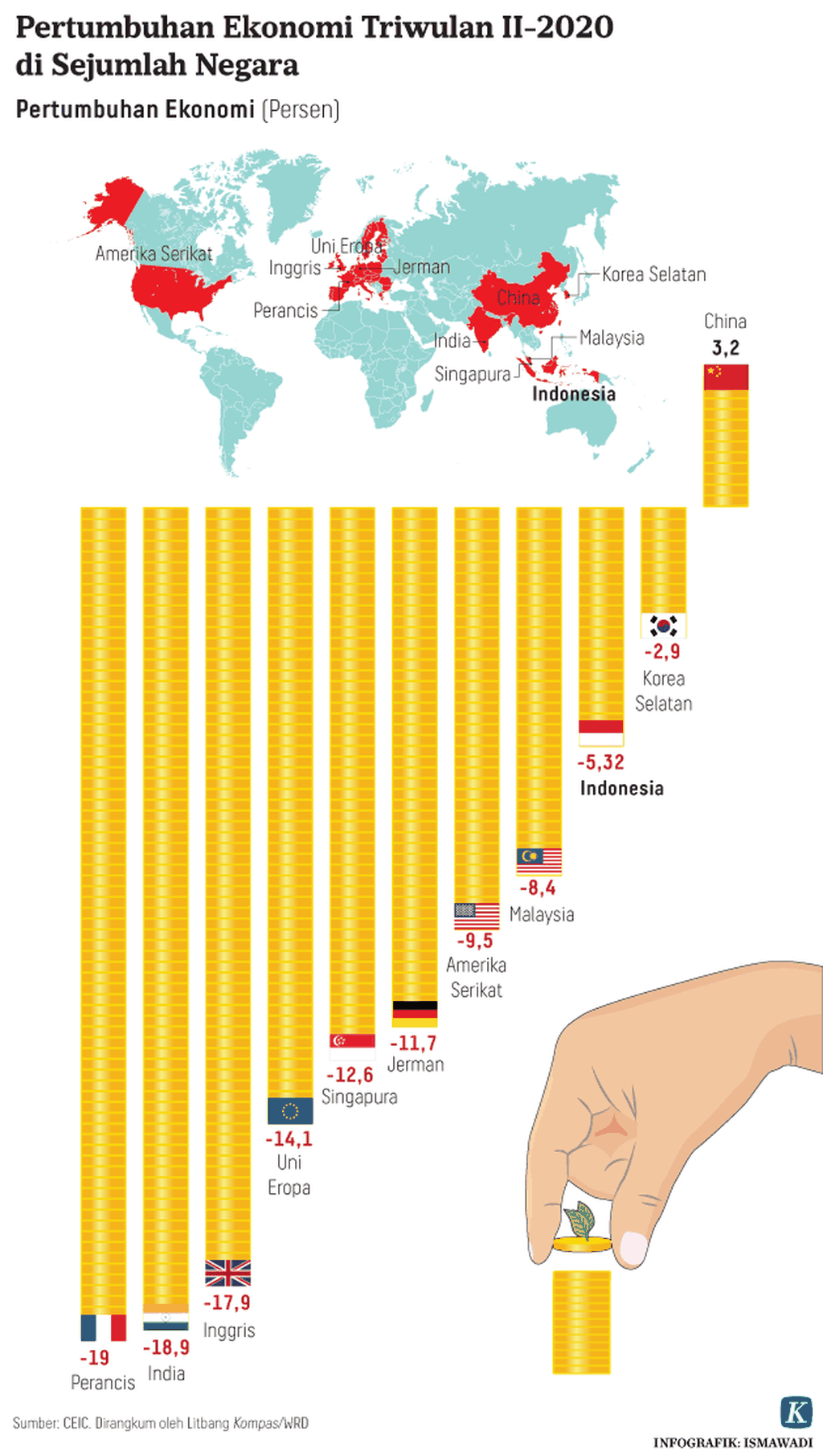

The threat of recession emerged after Statistics Indonesia (BPS) released an economic growth figure for the first six months of 2020, which contracted by 5.32 percent year-on-year (yoy). This is the first economic contraction since the economic crisis in 1998.

What is even more surprising is that in July 2020, it turned out that the Indonesian economy experienced deflation of 0.10 percent, therefore inflation in January to July 2020 was only 0.98 percent. The economic recession as a result of this pandemic has led to simultaneous deflation in several countries experiencing economic contraction. Singapore, Malaysia, and the Philippines are some examples of neighboring countries that have experienced deflation in recent months.

Also read : Notes for Recovering the Economy

This deflation was triggered by the falling prices of goods and services as a result of a contraction in the supply of money or credit in the economy. With the diminishing supply of money and credit, spending has been weak and investment has also stagnated. The potential for deflation in the following months will disrupt the handling Covid-19 and the recovery of the economy.

The prolonged economic crisis caused by the pandemic makes future deflationary opportunities even more difficult to predict. The emergence of deflation will make the threat of an economic recession worse. As an illustration, when we experienced an economic contraction as a result of the 1998 monetary crisis, we faced a very high inflation rate of 77.60 percent.

Also read : Recession and New Civilization

Second Quarter Economic Growth in Several Countries.

Risk due to deflation

The current deflation can be seen from the fall in prices of goods or services. The fall in secondary property prices and the current slowdown in new home sales are concrete examples that deflation has occurred in the field. A recent Bank Indonesia survey showed the volume of residential home sales during the second quarter of 2020 contracted by 25.60 percent (yoy).

In practice, the potential risk of loss as a result of deflation outweighs the benefits. Former Governor of the United States Federal Reserve, Ben S. Bernanke, said deflation should be avoided as much as possible because it has an extraordinary impact in the form of economic damage.

Prolonged deflation will pose various potential big risks that will worsen the condition of our economy, which is struggling to escape the threat of an economic recession. First, economic growth as measured by gross domestic product (GDP) from the demand side is highly dependent on spending and investment activities. Domestic spending has been the backbone of national economic growth and the emergence of deflation has reduced demand for goods and services.

Also read : Recession and Economic Sustainability

This condition will encourage entrepreneurs and factories to reduce production and cut production costs. This action will cause a domino effect, with the fall of supplies and prices of raw materials and other links that are part of the production process. Because the production sector cannot run its factory machines normally, a reduction in labor wages or a reduction in labor is a solution that must be chosen so that the risk of layoffs and unemployment is difficult to avoid.

Second, investment, which has been one of the engines of economic growth, will be disrupted. Entrepreneurs will rethink expansion or the procurement of new machines due to weak demand. For retail investors in the capital market, it is better to sell shares they own at a low price because the expected profit in the form of dividends to be obtained in the future from the corporation will experience a drastic decline, maybe even no dividends at all.

Also read : Indonesia to Mitigate Covid-19 Outbreak’s Economic Effects

A man is silhouetted against a monitor showing the Jakarta Composite Index (JCI) on Monday (2/3/2020) at the Jakarta Stock Exchange in South Jakarta. The JCI fell to 5,361 at the close of trade on Monday (2/3), weakening 1.68 percent from last week’s close following the government’s announcement of the first confirmed cases of COVID-19 infection in the country.

We can see how the Composite Stock Price Index (JCI), which has been decreasing for almost five months since the emergence of the Covid-19 pandemic, has not yet returned the figure before the pandemic.

Third, the prolonged deflationary condition has created uncertainty in the business world, resulting in banks pulling the brake on new credit disbursement. Banks prefer to invest in government bonds with fixed interest rates, which are much safer and more profitable. This condition makes it difficult for the business world to rise again due to the limited supply of working capital, which is mostly provided by banks. Without an injection of working capital from banks, it would be difficult for them to find other alternative sources of funding. Issuance of bonds as an alternative source of working capital funding cannot be not fully carried out by all corporations.

Also read : Driving the Economy Continuously

Fourth, deflation in the midst of threat of an economic recession as a result of Covid-19 is different from deflation that occurs when there is no economic crisis. The last deflation that occurred in February 2019 at 0.08 percent did not have a significant impact on the economy because at that time our economy was still growing positively and there was no crisis.

On the other hand, the current deflation not only reduces people\'s purchasing power due to the limited money they have, but also creates a psychological effect, namely the emergence of an extraordinary sense of fear due to the spread of the virus. For those who have enough or excess money, they are not necessarily able to spend the money. Social restrictions that occurred during the pandemic have reduced public consumption so that economic activity and production have been severely disrupted.

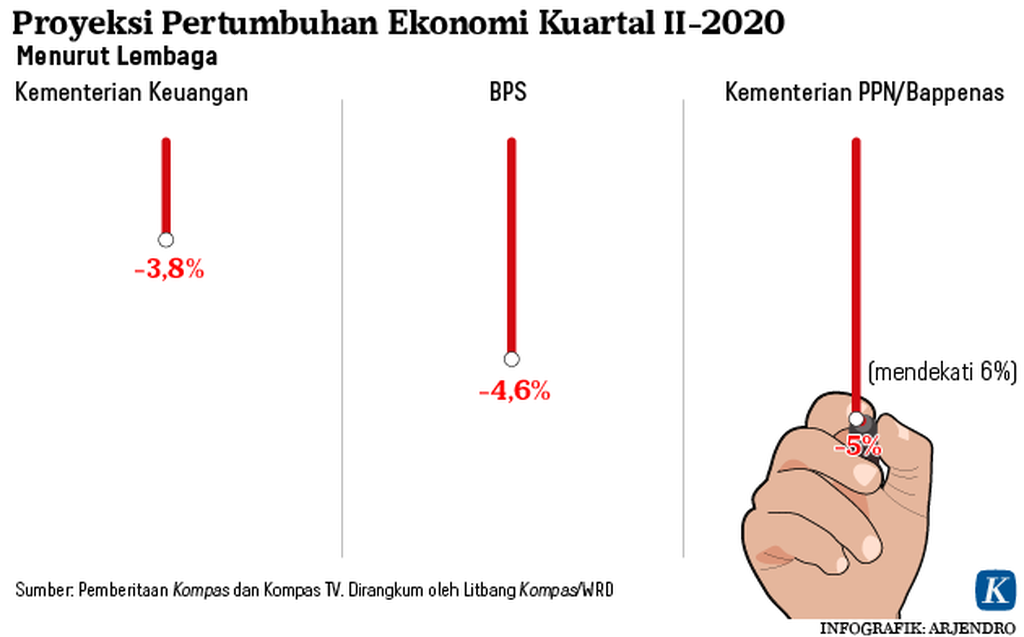

Projection of Indonesia\'s economic growth in the second quarter of 2020, according to; Ministry of Finance, Central Bureau of Statistics (BPS) and Ministry of PPN / Bappenas

Policy response

Many economists agree that preventing and overcoming inflation is theoretically easier than dealing with deflation. All existing forms of monetary and fiscal policy are usually aimed at suppressing the inflation rate so that it does not soar too high. Economists are also still debating whether the monetary and fiscal policies taken should be prioritized to prevent a recession or to prevent deflation.

An empirical study from Guerrero and Parker (2006) shows that deflation and economic recession have a causal relationship that influences each other. Therefore, we agree that macroeconomic policies must be prioritized to prevent economic recession because the success of these policies will automatically prevent prolonged economic deflation.

Also read : Revving the Engine of Economic Growth

Macroeconomic policies from the fiscal and monetary sides that have been carried out by the government in dealing with the pandemic and economic crisis are currently on the right track. Both the fiscal and monetary policies taken by the government have the same goal, namely to return liquidity to the real sector so that the economy is able to move back to normal. Therefore, macroeconomic policy is not only aimed at preventing an economic recession, but also must be able to prevent our economy from experiencing another deflation in the following months. It was enough for deflation to happen once in last July.

Even though the fiscal and monetary policies implemented by the government to date have been in the correct corridor, there is still an opportunity for the government to respond to deflation with further policies. First, increasing the tax rate on public savings in banks in order to boost the level of public consumption to a higher level.

Agus Sugiarto

People who have money today need to be encouraged to spend more so that the real sector is able to move again. Second, BI still has the opportunity to reduce the benchmark interest rate again, which is currently still at 4 percent, to a lower level in order to stimulate greater demand for credit. Third, people\'s business credit (KUR), which uses government funds with an interest rate of 6 percent, now needs to lower the interest rate again and also extend its tenor so that the micro and small business sector can obtain working capital with conditions that are not burdensome.

Agus Sugiarto, Advisor, Financial Service Authority.